User

Final response

CSI 300 & CSI 500 index futures term structure (2020–2026)

Methodology: 1,509 trading days (2 Jan 2020 – 27 Mar 2026) from connected exchange and market data feeds. Series include official CSI 300 and CSI 500 spot indices, continuous front- and next-month futures on each index, 3M funding as a risk-free proxy, and trailing 12-month realized dividend yields. Annualized basis: (F/S − 1) × 365/DTE with DTE ≤ 3 filtered to reduce expiry noise.

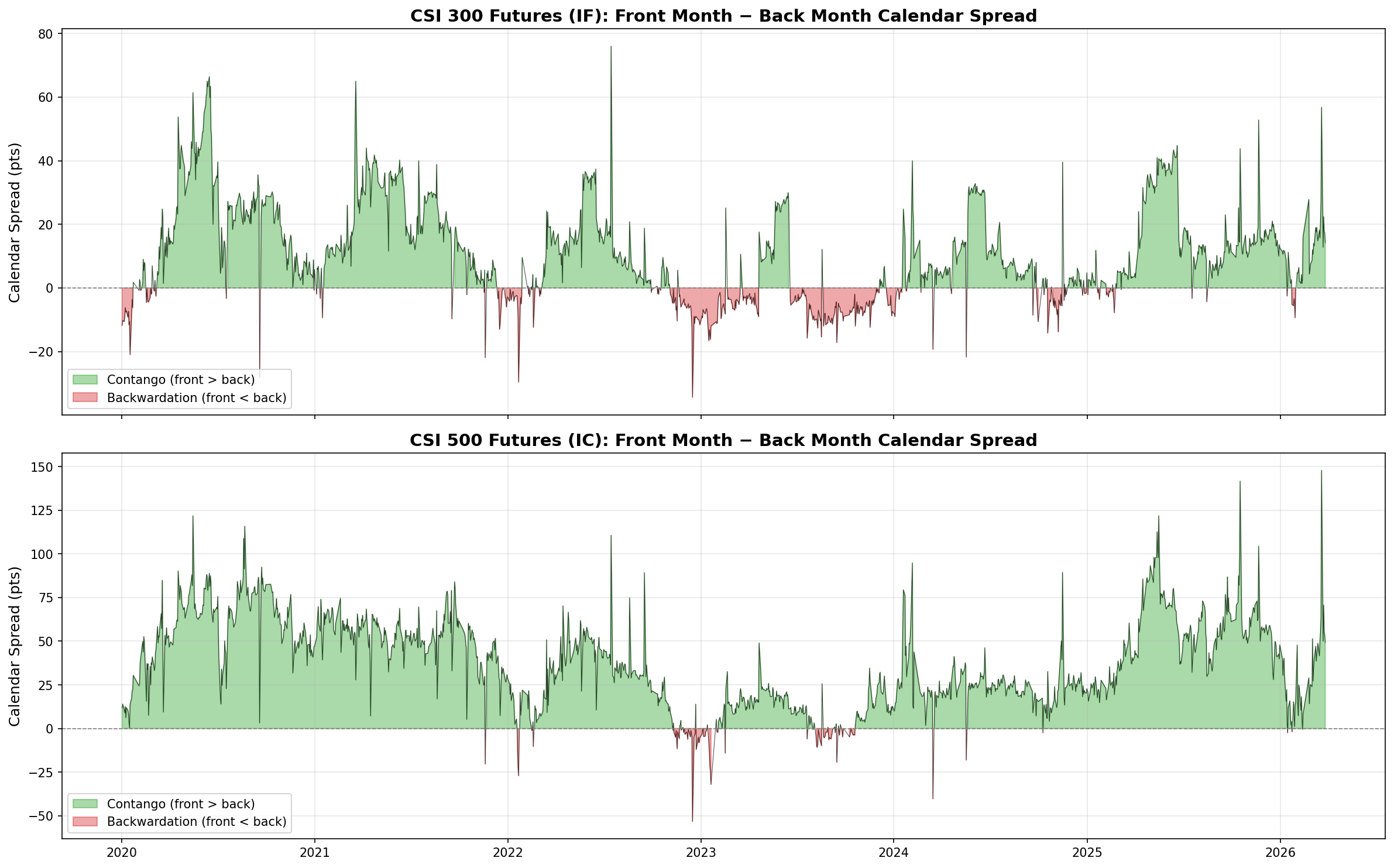

1. Calendar spread: front month − back month

Large-cap (CSI 300) vs mid-cap (CSI 500) calendar spreads — green = contango, red = backwardation.

Both legs skew toward backwardation (front above back) with sizeable variation. The CSI 500 contract is more volatile with wider negative spikes, consistent with heavier roll pressure from index hedgers.

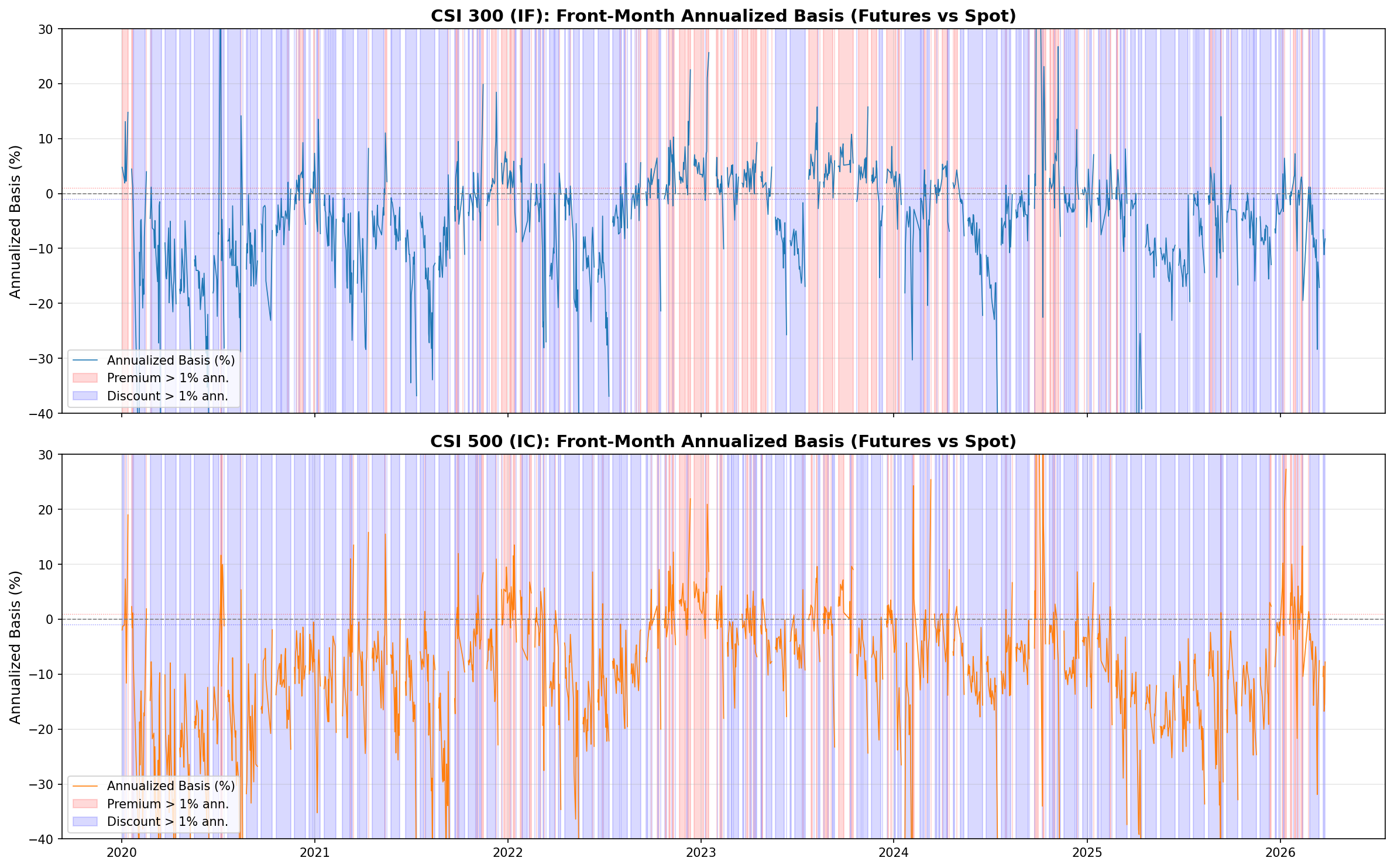

2. Annualized basis with premium / discount highlighting

Front-month annualized basis (%) with shading where premium or discount exceeds ±1% annualized.

| Metric | CSI 300 | CSI 500 |

|---|---|---|

| Mean annualized basis | −4.7% | −9.2% |

| Median annualized basis | −3.4% | −7.9% |

| Days in premium > 1% | 27.5% | 14.5% |

| Days in discount > 1% | 62.4% | 79.3% |

CSI 500 trades at roughly double the discount of CSI 300 — often linked to stronger hedging demand in the small/mid-cap sleeve.

3. Implied vs realized dividend yield

Implied dividend yield (from back-month basis + funding) vs trailing 12-month realized dividend yield.

| Metric | CSI 300 | CSI 500 |

|---|---|---|

| Mean implied div yield | 5.6% | 9.9% |

| Mean realized div yield | 2.6% | 1.6% |

| Excess (“hedging premium”) | +3.0% | +8.3% |

The gap is mostly structural hedging pressure, not dividend mis-estimation — especially the +8.3% wedge on the mid-cap leg.

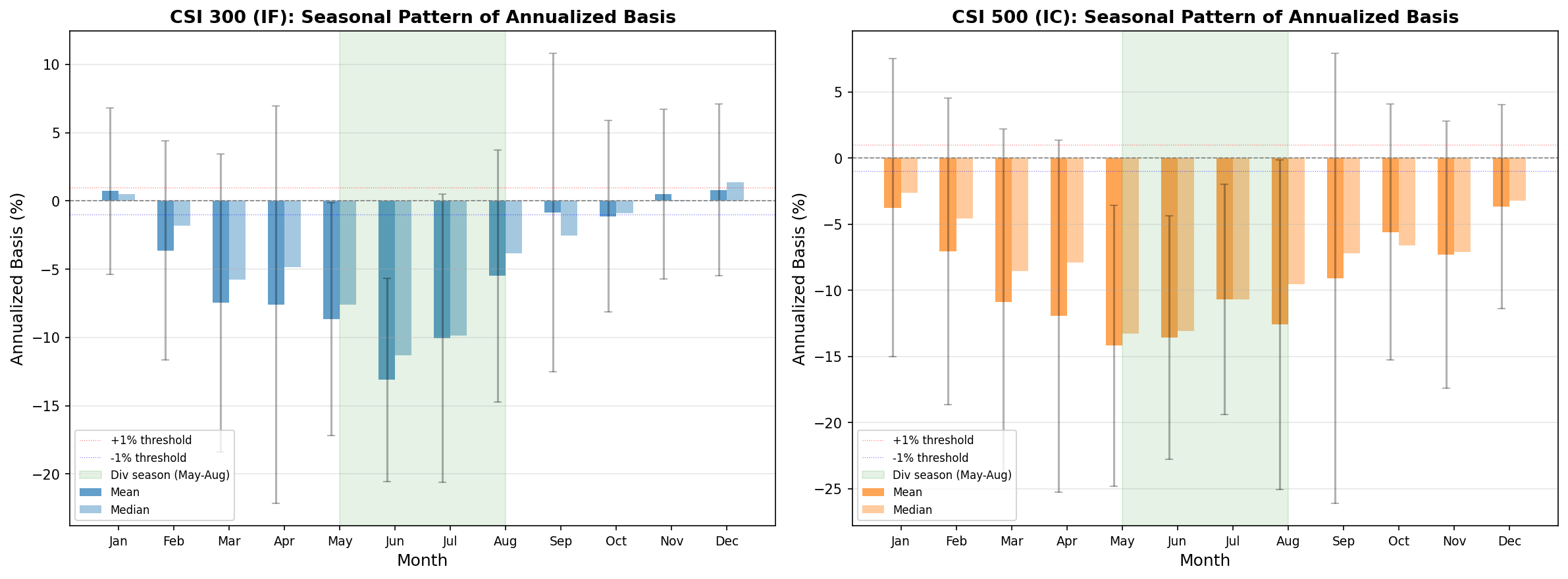

4. Seasonal pattern

Monthly pattern of annualized basis; shading marks dividend-heavy season (May–Aug).

| Month | CSI 300 mean basis | CSI 500 mean basis |

|---|---|---|

| Jan | +0.7% | −3.8% |

| May | −8.6% | −14.2% |

| Jun | −13.1% | −13.6% |

| Jul | −10.0% | −10.7% |

| Dec | +0.8% | −3.7% |

CSI 300 is weakest in June (dividend season); CSI 500 stays discounted for much of the year.

5. Year-by-year summary

| Year | CSI 300 basis (%) | CSI 500 basis (%) | 300 prem >1% | 300 disc >1% | 500 prem >1% | 500 disc >1% |

|---|---|---|---|---|---|---|

| 2020 | −9.4 | −17.4 | 13.8% | 80.5% | 5.1% | 93.3% |

| 2021 | −6.3 | −10.1 | 15.7% | 75.1% | 9.6% | 87.8% |

| 2022 | −4.1 | −6.1 | 33.0% | 53.1% | 27.3% | 64.4% |

| 2023 | +1.1 | −2.5 | 66.5% | 25.3% | 25.8% | 58.2% |

| 2024 | −2.5 | −6.6 | 28.6% | 60.3% | 10.6% | 82.9% |

| 2025 | −7.1 | −14.1 | 8.2% | 81.5% | 3.1% | 94.9% |

| 2026 YTD | −3.9 | −2.6 | 26.1% | 54.3% | 39.1% | 52.2% |

2023 stands out: CSI 300 mean basis turned positive with most days above +1% premium — often tied to lighter structured-product hedging flows, easier position limits, and more speculative long participation. Discounts returned in 2024–2025 as hedging activity picked up again.

Key takeaways

- CSI 500 > CSI 300 discount (~2×): structural hedging in small/mid-cap futures.

- Implied vs realized gap is largely a basis / short-hedging premium, not dividend forecasts alone.

- Seasonality: basis widens May–Aug (June trough for CSI 300), narrower Q4/Q1.

- Regime shift: 2023 CSI 300 premium episode was temporary; 2025–26 shows re-widened discounts, especially on CSI 500.